855-468-8900

Why Does Getting Life Insurance Take Time?

Insurance companies need lots of info to set your coverage price. They use different data to figure out where you stand on their actuarial table, which decides your insurance cost. Check out our guide on the ratings ladder below for more details.

Auto insurance companies quickly get all the info they need from state databases to check your driving history and set your price.

For life insurance, being young and healthy means insurers can quickly access your health info like MIB reports, prescription history, and sometimes lab results. This lets many offer fast services, even same-day coverage. But watch out—ads promising instant coverage often mean policies cost 30-50% more due to the speedy process.

If you're older or have conditions like diabetes, heart disease, or sleep apnea, getting life insurance can take longer because collecting medical records from your doctor(s) takes time. Thanks to HIPAA laws, your health information might be scattered across several places. Insurance companies often need 3-4 weeks or more just to gather your initial records.

Getting medical records takes time because they're often on paper and need to be copied and sent to the insurer. Doctor's offices use copy services for this task, which adds to the wait. Sometimes, you can get records through an online portal from your doctor, speeding things up, but these might not have all the details the insurance company needs, like specific test results.

Often, people in their 50s or 60s give their primary doctor's details to insurance companies, expecting that to cover all their medical history. However, if, for instance, you were referred for a sleep study and didn't follow up on the results, the insurance company will want to check this. They might wonder why it was recommended if you thought it wasn't a big deal. If the sleep study was normal, they need to know to avoid unnecessary rate changes. But not following up might seem like you're not taking doctor's advice seriously, which could affect your rates. It's crucial to clarify any medical recommendations with your doctor to ensure the insurance company has complete and accurate information. This is just one example of how detailed the underwriting process can be.

The outcome might be as quick as a call to your doctor or could extend to another 3-4 weeks for a response. This way, what starts as a 3-4 week process can stretch to 6-8 or even 12 weeks, even with the best intentions from both applicant and agent.

Clients often feel frustrated when asked for more doctor information a second time. It's common to hear concerns like "are they trying to decline me?" or doubts about health status not being clear from existing reports. Some might give up after a few weeks, feeling overwhelmed by the process.

Insurance companies and HassanHelps.com are keen to get you insured, which means it's vital to share your complete health and medical history, especially from the last decade. This thoroughness not only speeds up the underwriting process but also ensures your coverage fits your needs accurately.

Life insurance policies have a 2-year contestability period for challenging claims, primarily due to undisclosed health information. Not mentioning you're on cholesterol meds might not affect your claim, but overlooking to disclose something like marijuana use or a significant health event such as a triple bypass could lead to claim disputes or adjustments in your policy's benefits. This could negatively impact your beneficiaries.

The aim is to gather all relevant information upfront to make the approval process smoother and faster, ensuring your policy accurately represents your health status. This detailed approach helps in protecting your beneficiaries effectively and aligns with the insurer's need to assess risks accurately. Every question we ask is designed to secure the best insurance coverage for you.

What Rate Class Will You Qualify For?

(General Guidelines - Expect Exceptions & HassanHelps Finds Them)

The Ratings Ladder

Your Life Insurance rating isn't just about negotiating. Today, insurance companies can access extensive details about your health, including doctor's records, lab results, prescription history, and your MIB (Medical Information Bureau) report. With data from millions over the years, insurers know which health factors pose more risk. They use this info to determine your insurance rate. Sometimes, underwriters might not get it right and quote you too high; that's when HassanHelps.com steps in to ensure your health profile is accurately represented. Insurance companies each have their own criteria and specializations—some may offer better rates for conditions like diabetes or sleep apnea. Our job is to find the right match for you.

HassanHelps.com Excels At Matching You With The Ideal Insurance Company.

After reviewing your health, the underwriter assigns you a spot on what we call the "Ratings Ladder," with 12 levels—1 being the cheapest, 12 the most expensive. Each age and gender has its own ladder, so all 50-year-old men are on one ladder, while 50-year-old women have theirs. Everyone starts at Standard Rate, which is rung 4. Your health details can move you up or down this ladder. For example, a diabetic might start at rung 6, but good management of their condition could bring them down to rung 3 or 4. Our role at HassanHelps.com is to work with the underwriter, highlighting the positives in your health to ensure you land on the lowest possible rung.

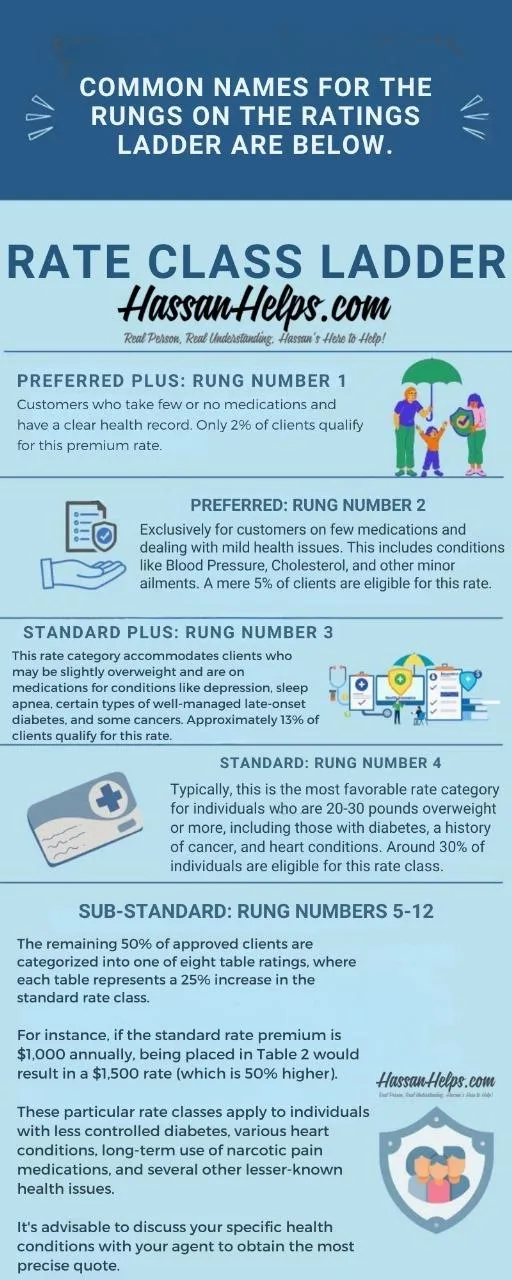

Here Are The Common Names For Each Level On The Ratings Ladder.

Preferred Plus. Rung number 1

Clients on few medications with no major health history. Only 2% get this rate.

Preferred Plus. Rung number 2

For clients with minimal meds and mild conditions like blood pressure or cholesterol. Only 5% qualify for this rate.

Standard Plus. Rung Number 3

A bit overweight? Taking meds for depression, sleep apnea, controlled diabetes or cancer? 13% get this rate.

Standard Plus. Rung Number 4

20-30+ lbs overweight? Diabetes, cancer history, heart conditions? This is usually the best rate for 30% of people.

Table Ratings. Rung Numbers 5-12

The other 50% fall into 1 of 8 table ratings, each adding 25% to the standard rate. E.g., a $1000 standard premium becomes $1500 for Table 2. These cover less-controlled diabetes, heart conditions, long-term narcotic use, and more. Discuss your specific health conditions with your agent for an accurate quote.

Get Your Free Life Insurance Quote Now

About Us

TermLifeProvider | Home of HassanHelps is a leading life insurance brokerage with the best rates from top insurers. With over 16 years, we've helped thousands save on life insurance.

We've seen many clients struggle with weight and related health issues like sleep apnea, diabetes, high blood pressure, arthritis, and heart disease. By educating our clients on how these health issues affect life insurance costs, we aim to improve their health and reduce their premiums.

© 2025 HassanHelps.com